Not too long ago, envisioning a cashless financial system in a remarkably diverse and expansive nation like India seemed like an impossible dream. Skeptics frequently questioned how a largely cash-dependent society—especially rural citizens and small-scale vendors—could seamlessly transition to digital payments. Fast forward to the present, and the Unified Payments Interface (UPI) has silenced those doubts, turning smartphones into pocket-sized banks and fundamentally rewiring the nation’s economy.

Overcoming the Hurdles of Traditional Banking

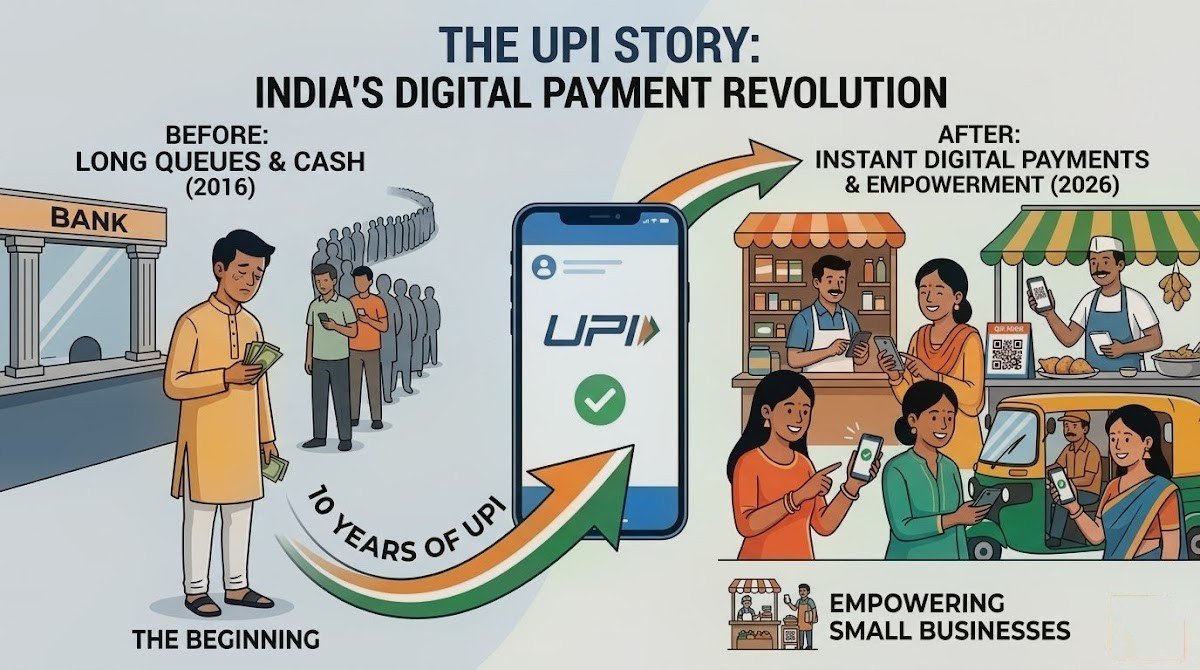

To truly appreciate the magnitude of India’s digital leap, it is essential to look at the financial landscape of the past. For decades, routine banking tasks, such as transferring funds or paying utility bills, were synonymous with tedious paperwork and long hours spent in queues. Rural demographics were particularly marginalized due to a severe lack of local bank branches and ATMs. Although early digital mechanisms like RTGS (2004) and IMPS (2010) were introduced, their benefits were largely restricted to individuals who already had established footprints within the formal banking sector.

The Foundation of Financial Inclusion: The JAM Trinity

The true turning point for universal digital adoption was the strategic rollout of the “JAM Trinity,” a unified framework consisting of three key pillars:

Jan Dhan Accounts: A massive financial inclusion initiative that successfully opened zero-balance bank accounts for hundreds of millions of previously unbanked individuals.

Aadhaar: A biometric identification system that provided a unique, verifiable digital identity to nearly every Indian citizen.

Mobile Connectivity: The technological bridge that linked a citizen’s identity directly to their financial assets.

This robust infrastructure paved the way for the Direct Benefit Transfer (DBT) system. By routing government subsidies and welfare funds directly into citizens’ accounts, the system effectively eliminated intermediaries, curbed systemic corruption, and fostered immense public confidence in digital governance.

2016: The Digital Paradigm Shift

The financial ecosystem experienced a seismic shift with the launch of UPI in 2016. This platform stripped away the complexities of traditional online banking. Users no longer needed to memorize cumbersome account details or IFSC codes; a simple virtual ID or linked phone number was enough to facilitate instant, round-the-clock money transfers. Furthermore, its inherent interoperability meant that users could effortlessly transfer funds across a multitude of competing banking applications.

Scaling Unprecedented Heights

The statistical growth of this platform highlights a narrative of unprecedented economic momentum. By January 2026, the network processed an astonishing 21.7 billion transactions in a single month, representing a financial value of approximately ₹28.5 lakh crore. Today, India facilitates nearly half (49%) of all real-time digital payments across the globe. The underlying infrastructure has grown proportionally, expanding from roughly 200 participating banks in 2021 to nearly 700 by 2026.

Empowering the Grassroots Economy

The most profound triumph of this technology lies in its grassroots adoption. From metropolitan retail hubs to village vegetable carts, QR codes have become a universal medium of exchange. This transition has completely eradicated the daily friction of managing physical cash and exact change. More crucially, it has allowed micro-entrepreneurs and street vendors to generate verifiable digital transaction histories. Armed with this data, these small business owners can now access formal credit and loans that traditional banking systems previously denied them.

Taking Indian Technology Global

India has successfully transitioned from being a consumer of foreign technology to an exporter of digital public infrastructure. The seamless payment model has gained immense international traction, with active integrations in nations such as Singapore, the UAE, France, Nepal, and Bhutan. This global footprint allows Indian travelers to make instantaneous, rupee-denominated transactions at international landmarks, including the Eiffel Tower.

Charting the Financial Future

The ecosystem continues to innovate at a rapid pace. The introduction of features like ‘Lite’ versions for micro-transactions, automated recurring payments, and direct access to credit lines demonstrates a shift from a simple payment gateway to a comprehensive financial services hub. Backed by stringent two-factor authentication protocols, the network maintains rigorous security standards.

The journey from endless banking queues to instantaneous QR code scans is far more than a technological upgrade; it is a story of profound socio-economic empowerment. It stands as a powerful global case study on how accessible, well-designed digital infrastructure can democratize finance and uplift an entire nation.