People from India who work in other countries send a massive amount of money back home to their families. In fact, India receives more of this money than any other country in the world. For decades, workers have used regular banks and official money transfer services to send this cash. But today, a hidden shift is happening. Many people are skipping the banks and using a type of digital money called “stablecoins” instead.

What is a Stablecoin?

You might have heard of cryptocurrencies like Bitcoin, whose value jumps up and down every day. A stablecoin is different. Its value is locked to real-world money, so it stays steady.

The most famous example is a coin called Tether (USDT). Tether is tied directly to the US Dollar. This means one USDT is designed to be worth exactly one US Dollar.

Why are People Switching to Digital Coins?

Right now, billions of dollars are flowing into India through these digital coins. People are making the switch for a few major reasons:

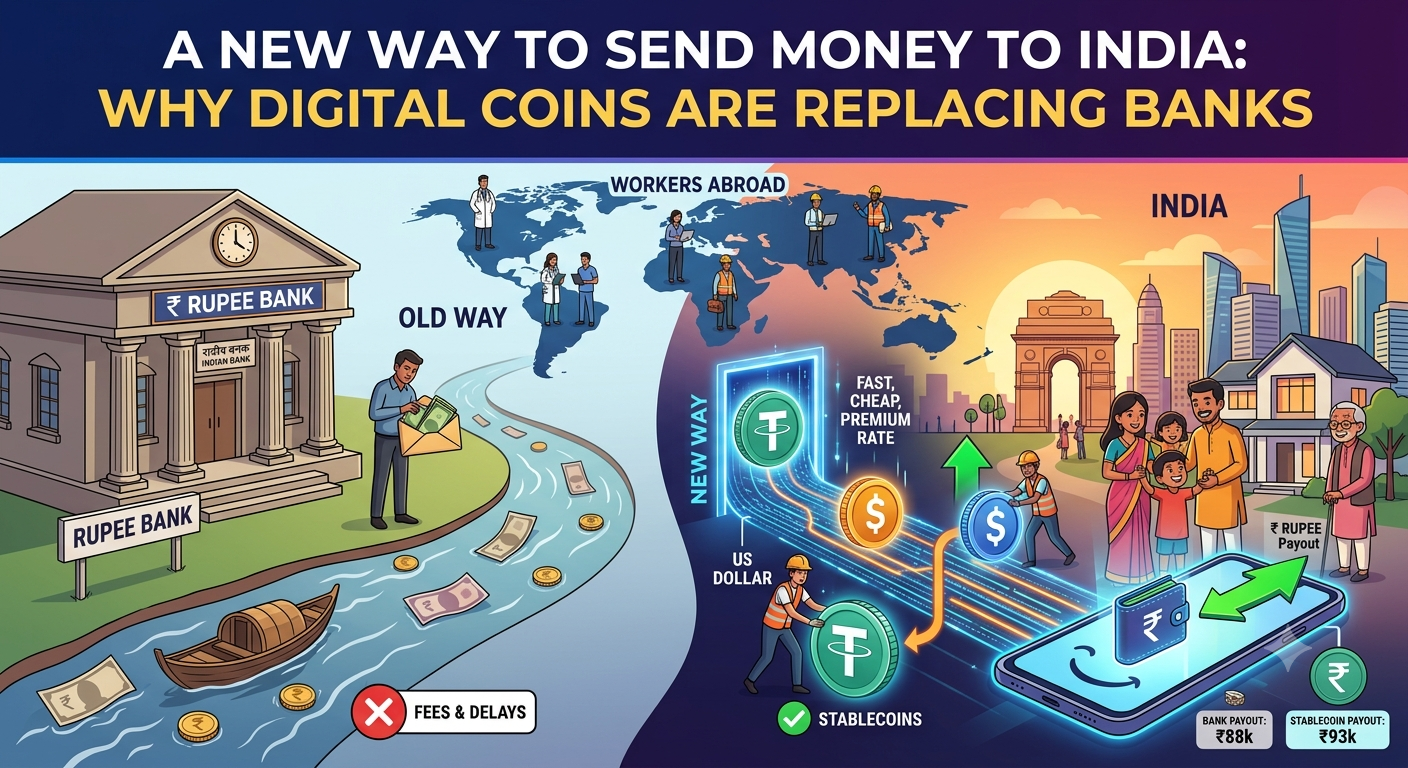

Bigger Payouts: This is the main reason people use stablecoins. If a worker sends $1,000 through a regular bank, the bank uses the official exchange rate, and the family might get around ₹88,600. However, in India’s unofficial digital markets, stablecoins are in very high demand. Because of this demand, local buyers are willing to pay extra for them. If the worker sends 1,000 USDT instead, the family can sell it and might get around ₹93,000.

Faster and Cheaper: Sending money through a bank can take anywhere from one to three days, and the bank takes a cut of the money as a fee. Sending a stablecoin is almost instant and costs practically nothing.

How Do They Do It?

The process is surprisingly simple:

A worker living abroad takes their dollars and buys USDT online.

They send that digital money directly to a local broker’s digital wallet in India.

The family in India goes to that broker and collects the cash in Rupees at the higher, unofficial rate.

The Hidden Dangers

While this sounds like a great deal for the sender, it creates massive problems for the country. The government and the Reserve Bank of India (RBI) do not track or approve of these private digital transfers. This leads to several major risks:

- Funding Crime: Because these transactions are invisible to the government, it makes it incredibly easy for criminals or terrorist groups to move large amounts of illegal money.

- Avoiding Taxes: The government usually takes a small tax on digital trades. By doing this in secret, people are dodging their taxes.

- Risk of Getting Scammed: If the local broker decides to steal the digital money and disappear, the family is out of luck. Because it is unofficial, the police and the RBI cannot help them get their money back.

- Losing Economic Control: The RBI is supposed to manage the country’s money supply to keep the economy healthy. If everyone starts using unregulated digital dollars instead of Rupees, the government loses its ability to control the economy.

What Happens Next?

Around the world, stablecoins are becoming so popular that they are now processing more daily transactions than major credit card companies like Visa.

Since it is almost impossible to completely ban these hidden transfers, India will likely have to find a way to regulate them. Experts suggest that the government might need to start giving out official licenses to trusted digital brokers. By creating rules and perhaps linking these transfers to India’s own official digital currency (the e-Rupee), the government could make the system safer and bring this hidden money back into the light.